Inference for a Single Proportion

Math 215

Two data sets

We will consider two data sets:

- First is on payday loan regulations in MI (

payday) - Second is on the complication rate for liver donor surgeries in the U.S. (

consult)

- First is on payday loan regulations in MI (

We will use the first data set as an example of an inference based on a mathematical model and second as an example of a simulation based inference

The decision in each case is based on the success-failure condition of the Central Limit Theorem

Mathematical Model for a Proportion

- We have learned that if certain conditions are met we can use a mathematical model to make inferences about a population

- There is a version of the Central Limit Theorem for a single proportion

Sampling distribution of \(\hat{p}\)

The sampling distribution of \(\hat{p}\) based on a sample of size \(n\) from a poplation with true proportion \(p\) will be approximately normal with mean \(p\) and standard error \[SE=\sqrt{\frac{p(1-p)}{n}}\]

if the following technical conditions are met:

- independent observations (e.g., observations from SRS)

- (success-failure condition) at least 10 expected successes and at least 10 expected failures. (i.e., \(np\geq 10\) and \(n(1-p)\geq 10\))

Payday Loan Regulations

- Borrowers use payday loans to get a cash advance before their next payday

- Borrower writes a check for loan amount + service fee

- Lender holds check until borrower’s payday

- Very high APR equivalent (often over 300%)

- Some borrowers take out second loan to pay of first, and so on

- Michigan already has a law that limits the number of payday loans a borrower can hold (2)

- Do most payday borrowers support additional regulation that would require payday lenders to do a credit check?

- Let \(p\) be the long-run proportion of all payday borrowers in MI that support additional regulation.

- Note that \(p\) represents a population parameter

Hypotheses

In words:

\(H_0:\) the proportion of all payday borrowers in MI that support additional regulation is 50%.

\(H_A:\) The majority of all payday borrowers (more than 50%) in MI that support additional regulation.

In symbols:

\(H_0: p = 0.5\)

\(H_A: p > 0.5\)

Data

paydaydata set- Researchers selected a random sample of 826 payday borrowers

- 424 (51.3%) said they would support a regulation

- \(\hat{p}=0.513\)

- The success-failure condition is met:

- Under the null hypothesis, we expect \(n\times p=0.5\times 826 = 413\) people to support the legislation

- \(n\times (1-p)=(1-0.5)\times 826 = 413\) to not support the legislation.

- It is appropriate to model the null distribution using a normal distribution

Hypothesis Test Using Normal Approximation

- The standard error, according to the CLT is \[SE(\hat{p})=\sqrt{p_0(1-p_0)/n}\] Where \(p_0\) is the proportion under the null hypothesis

- We will use the Z score as the test statistic

\[Z = \frac{\hat{p}-p_0}{SE(\hat{p})}=\frac{\hat{p}-p_0}{\sqrt{p_0(1-p_0)/n}}\]

- Recall that if \(\hat{p}\) is normally distributed, then \(Z\) has a standard normal distribution, \(N(0,1)\)

- For the payday study \(p_0=0.5\), and \(\hat{p}=0.513\), so \[SE(\hat{p})=\sqrt{p_0(1-p_0)/n}=\sqrt{0.5\cdot(1-0.5)/826}=0.0174\]

- So the z-score is \[Z = \frac{0.513 - 0.5}{0.0174}=0.765\]

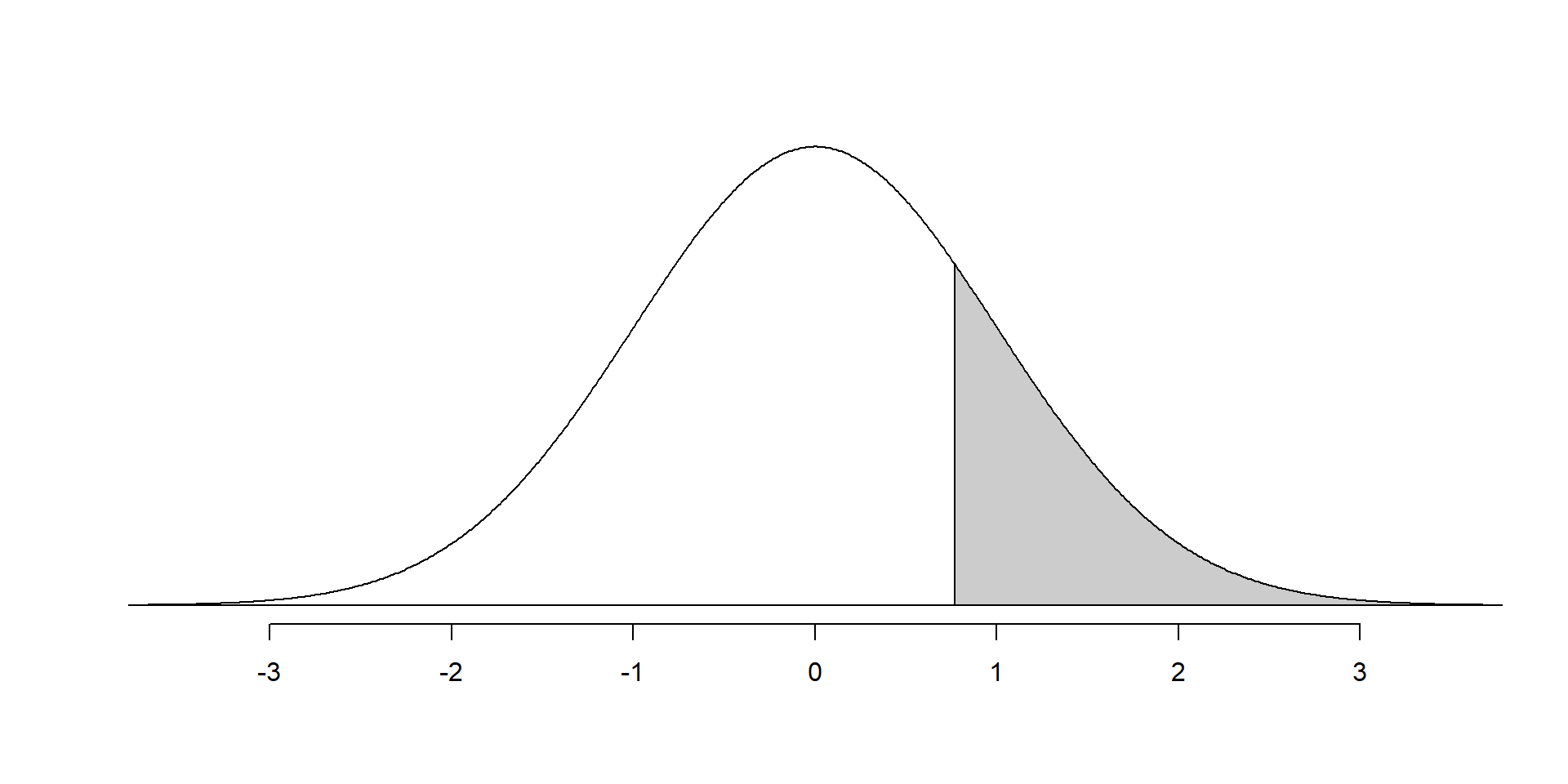

- The p-value is the probability that we would obtain a \(Z\) score at least as large as 0.765 if the null hypothesis is true

- We compute the p-value by finding the area under the density curve for \(N(0,1)\) that is beyond 0.765

Normal model, \(N(0,1)\). P-value is area of shaded region.

- We are unable to reject the null hypothesis (p-value = 0.22)

- Therefore, 50% is a plausible value for the parameter

- Note that we cannot claim that 50% of payday borrowers support the new legislation (we cannot accept the null hypothesis)

- We state that we failed to reject null hypothesis

Confidence Interval

- We can also use a normal distribution to find a confidence interval if technical conditions are met

- Earlier we used \(p_0\) as the mean and in the computation of SE, because we were trying to approximate the null distribution

- A confidence interval estimates the value of the parameter, so it only can rely on the sample data

- The best point-estimate we have is the sample proportion \(\hat{p}\), so we use that in the computation of SE

Checking Conditions for CI

- The success-failure condition is easier to check in this situation.

- \(n\hat{p}\) is the number of observed success, and \(n(1-\hat{p})\) is the number of observed failures.

- We just need to check if there were 10 successes and 10 failures in the sample.

- For the Payday loans study, the success-failure condition is met. There were 424 successes and 402 failures

- It is appropriate to use a normal approximation to find a CI

Confidence Interval Using a Normal Approximation

- If a normal approximation is appropriate, a confidence interval for a proportion can be written as \[\hat{p}\pm z^{\ast}\times SE\]

- SE is estimated using \[SE\approx\sqrt{\frac{\hat{p}(1-\hat{p})}{n}}\]

- \(z^{\ast}\) is determined by the confidence level (e.g., 1.645 for 90%, 1.96 for 95%, 2.576 for 99%)

- The standard error for the proportion of borrowers that support the new regulation is \[SE \approx \sqrt{\frac{0.513\cdot(1-0.513)}{826}}=0.0174\]

- The 95% confidence interval is \[0.513\pm1.96\cdot0.0174 = 0.513\pm0.034\]

- We are 95% confident that the long-run (or true) proportion of all payday borrowers that support the new regulation is between 0.479 and 0.547

- Note that value 0.5 used previously in the null hypohesis is inside of the 95% confidence interval, conforming the fact that 50% is a plausible value for the parameter

Simulation Based Inference

Medical Consultants

- Some organ donors work with a medical consultant who helps them throughout the process

- The average complication rate for liver donor surgeries in the United States is about 15%

- One consultant claims she has low rate of complications compared to national average.

Is her claim supported?

- Let \(p\) be the consultant’s long-run complication rate

Hypotheses:

- \(H_0: p = 0.15\)

- \(H_A: p < 0.15\)

Data:

consultdataset- She has served as a consultant for 62 liver donor surgeries

- 3 (4.8%) resulted in complications

- \(\hat{p} = 0.048\)

Checking Technical Conditions

Consultant study

- The success-failure condition is not met. Under the null hypothesis, we expect \(62\times 0.15 = 9.3\) complications (less than 10)

- Cannot model null distribution using a normal distribution

- Use randomization instead (parametric bootstrap simulation)

Hypothesis Test Using Randomization

- In the consultant study we cannot use a normal model for the null distribution

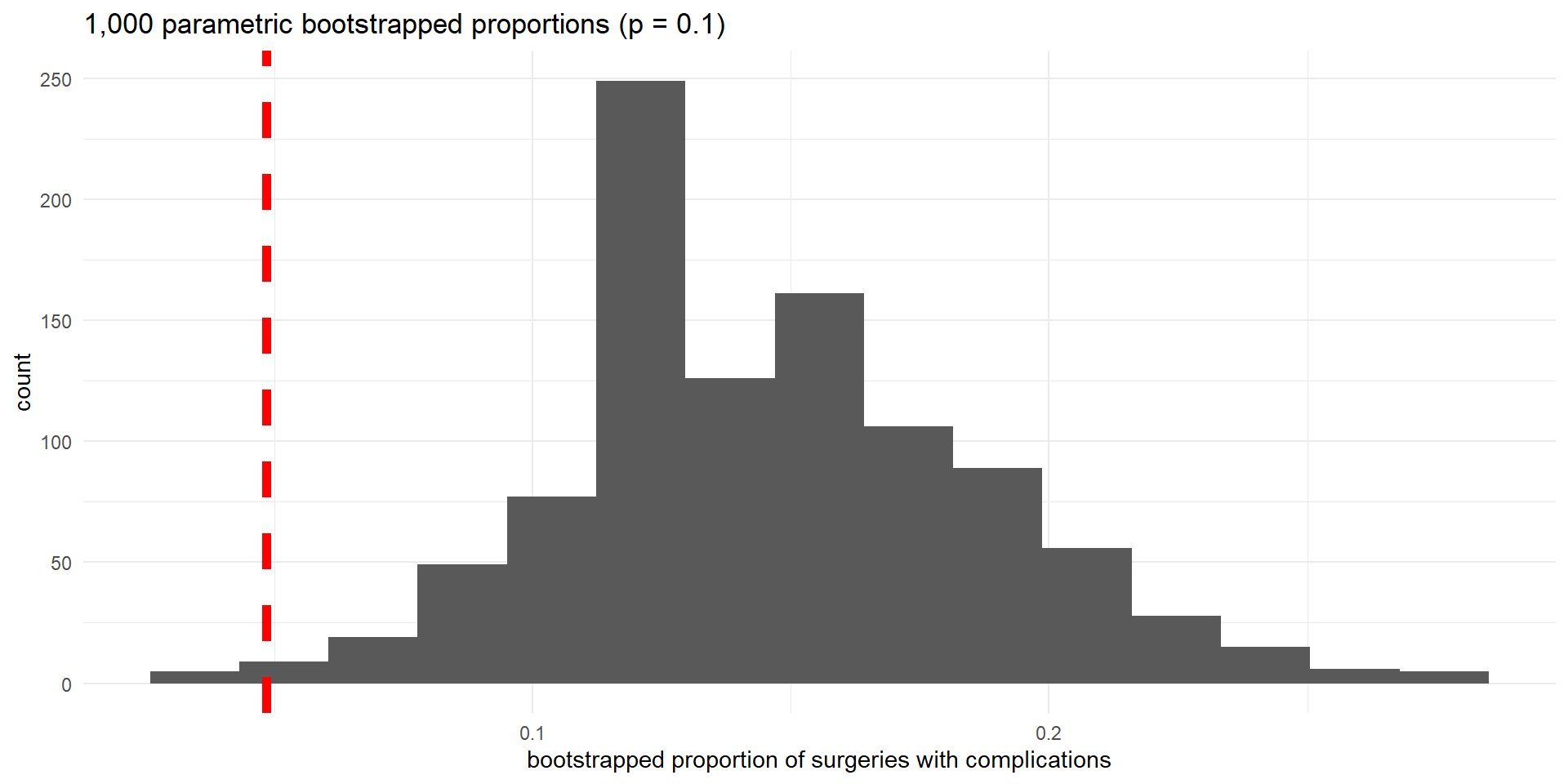

- However, we can use parametric bootstrap simulation to approximate the null distribution

- We simulate 1,000 random samples of 62 liver donors from a population in which the null hypothesis is true (10% complication rate)

Parametric bootstrap simulation is equivalent to the following physical simulation:

- For each donor simulate the outcome by spinning a spinner with 15% of the area representing “complication” and 85% representing “no complication”

- For each sample, spin the spinner 62 times (sample size) and record the proportion of complications in the sample

- Repeat to obtain proportions for 1,000 simulated samples

We can do the bootstrapping using the infer package

- The p-value is approximated by the proportion of bootstrapped proportions that are at least as extreme as the observed proportion (\(\leq 0.048\))

# A tibble: 1 × 2

n_extreme p_val

<int> <dbl>

1 14 0.014- With a p-value of 0.014 we reject the null hypothesis.

- We have strong confidence that the consultant has complication rate lower than 15%

Checking Conditions for CI

- For the Consultant study, the success-failure condition is not met. There were 3 successes and 59 failures

- Cannot use normal approximation to find a CI

- Use randomization instead (bootstrap as in Chapter 12)

Confidence Interval Using a Bootstrapping

- We use bootstrapping to find a 95% confidence interval for the complication rate for the medical consultant

- This time we take repeated samples (with replacement) from our original sample

- The 95 % bootstrap confidence interval is obtained by calculating the 2.5% and 97.5% percentiles for the bootstrapped statistics.

# A tibble: 1 × 2

ci_lo ci_hi

<dbl> <dbl>

1 0 0.113- We are 95% confident that the consultant’s long-run complication rate is between 0 and 0.113

- Note that the value we used in the null hypothesis (0.15) is not in the confidence interval, confirming that we rejected 15% as a plausible value for the parameter of interest