# A tibble: 4 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 4.31 0.195 22.1 2.09e-105

2 debt_to_income 0.0408 0.00307 13.3 4.76e- 40

3 term 0.158 0.00417 37.9 6.24e-294

4 credit_checks 0.247 0.0193 12.8 3.29e- 37Inference: Multiple Regression

IMS1 Ch. 25

Math 215

Yurk

Interest Rates

loans1- 10,000 loans through Lending Club, individuals lend to each other

- Response:

interest_rate - Predictors:

dept_to_income(debt to income ratio),term(number of months for loan),credit_checks(number of credit inquiries in last 12 months)

Multiple Regression Output

Linear model: \[\begin{array}{rcl}\widehat{interest\_rate} &=& 4.31+0.0408\times debt\_to\_income\\ &+& 0.158 \times term +0.247\times credit\_checks\end{array}\]

# A tibble: 4 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 4.31 0.195 22.1 2.09e-105

2 debt_to_income 0.0408 0.00307 13.3 4.76e- 40

3 term 0.158 0.00417 37.9 6.24e-294

4 credit_checks 0.247 0.0193 12.8 3.29e- 37- A standard error and \(T\)-statistic is listed for each coefficient

- We will not discuss the details of the standard error calculation (linear algebra)

# A tibble: 4 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 4.31 0.195 22.1 2.09e-105

2 debt_to_income 0.0408 0.00307 13.3 4.76e- 40

3 term 0.158 0.00417 37.9 6.24e-294

4 credit_checks 0.247 0.0193 12.8 3.29e- 37- Hypothesis test for coefficient for each predictor:

- \(H_0: \beta_1=0\), given

termandcredit_checksincluded in the model - \(H_0: \beta_2=0\), given

debt_to_incomeandcredit_checksincluded in the model - \(H_0: \beta_3=0\), given

debt_to_incomeandtermincluded in the model

- \(H_0: \beta_1=0\), given

- For \(k\) predictors, \(df=n-k-1\)

# A tibble: 4 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 4.31 0.195 22.1 2.09e-105

2 debt_to_income 0.0408 0.00307 13.3 4.76e- 40

3 term 0.158 0.00417 37.9 6.24e-294

4 credit_checks 0.247 0.0193 12.8 3.29e- 37- All three coefficients are significant

- For example, it would be extremely unlikely to obtain a value for the

debt_to_incomecoefficient that is at least as extreme as 0.0408 if there is no relationship between interest rate an debt to income ratio

Interpreting Coefficients

# A tibble: 4 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 4.31 0.195 22.1 2.09e-105

2 debt_to_income 0.0408 0.00307 13.3 4.76e- 40

3 term 0.158 0.00417 37.9 6.24e-294

4 credit_checks 0.247 0.0193 12.8 3.29e- 37- The model predicts that interest rate will increase by 0.0408 for each increase of 1 in the debt to income ration (assuming the other predictors are held constant)

- Interest rate is predicted to increase by 0.247 for each additional credit check

- Does this mean that credit checks are more important than debt to income ratio?

It is not informative to compare coefficient values when the data are on different scales

| predictor | mean | sd |

|---|---|---|

debt_to_income |

19.3 | 15.0 |

term |

43.3 | 36 |

credit_checks |

1.96 | 2.3 |

Standardized Predictors

- We can standardize the predictors by calculating the number of standard deviations each value is from the mean

- The \(i\)th observation of the \(j\)th predictor \(x_j\) is standardized as \[u_{ij}=\frac{x_{ij}-\bar{x}_j}{s_j}\]

- The standardized predictors have mean = 0, standard deviation = 1

- Let’s standardize the predictors for the interest rate example

- We can use the

mutatefunction

loans_standardized <- loans |>

mutate(debt_to_income =

(debt_to_income - mean(debt_to_income, na.rm = TRUE))/

sd(debt_to_income, na.rm = TRUE)) |>

mutate(term =

(term - mean(term, na.rm = TRUE))/

sd(term, na.rm = TRUE)) |>

mutate(credit_checks =

(credit_checks - mean(credit_checks, na.rm = TRUE))/

sd(credit_checks, na.rm = TRUE))# A tibble: 4 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 12.4 0.0459 270. 0

2 debt_to_income 0.612 0.0460 13.3 4.76e- 40

3 term 1.74 0.0460 37.9 6.24e-294

4 credit_checks 0.588 0.0460 12.8 3.29e- 37- The intercept is the predicted interest rate when each of the predictors have their mean value

- If debt to income ratio is increased by 1 standard deviations, interest rate is predicted to increase by 0.612 (holding other predictors constant)

- Similar interpretation for other coefficients

# A tibble: 4 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 12.4 0.0459 270. 0

2 debt_to_income 0.612 0.0460 13.3 4.76e- 40

3 term 1.74 0.0460 37.9 6.24e-294

4 credit_checks 0.588 0.0460 12.8 3.29e- 37- Since all predictors are on the same scale, coefficient comparisons are more meaningful

- E.g.,

termhas the largest impact on predictedinterest_rate - p-values have not changed

Coins

- Next we explore the

moneydata set - Amount of money in different people’s coin dishes (simulated data)

- Response:

total_amount(USD) - Predictors:

number_of_coins,number_of_low_coins(pennies, nickels, dimes) - We will use this dataset to explore multiple linear regression with correlated predictors

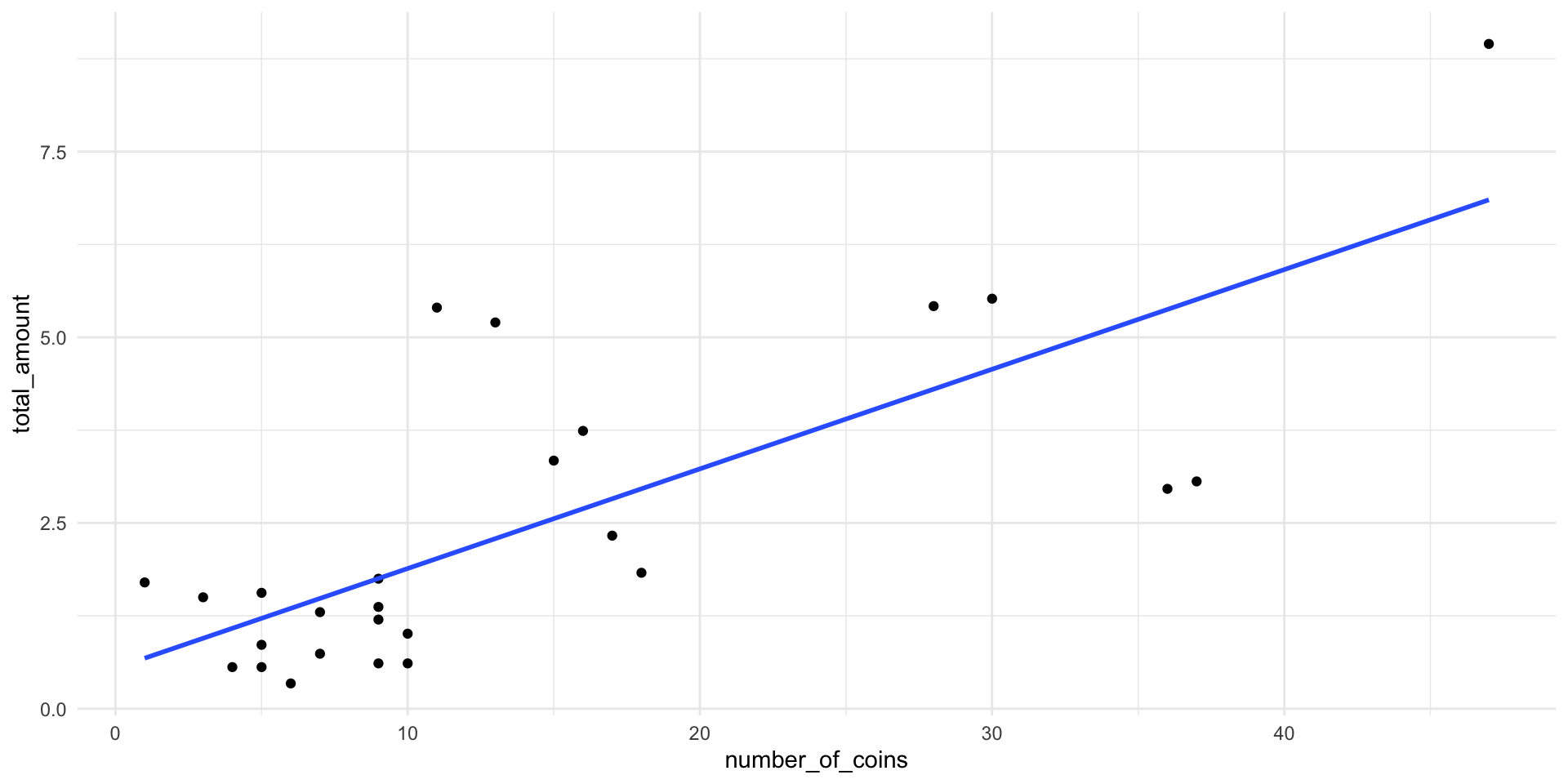

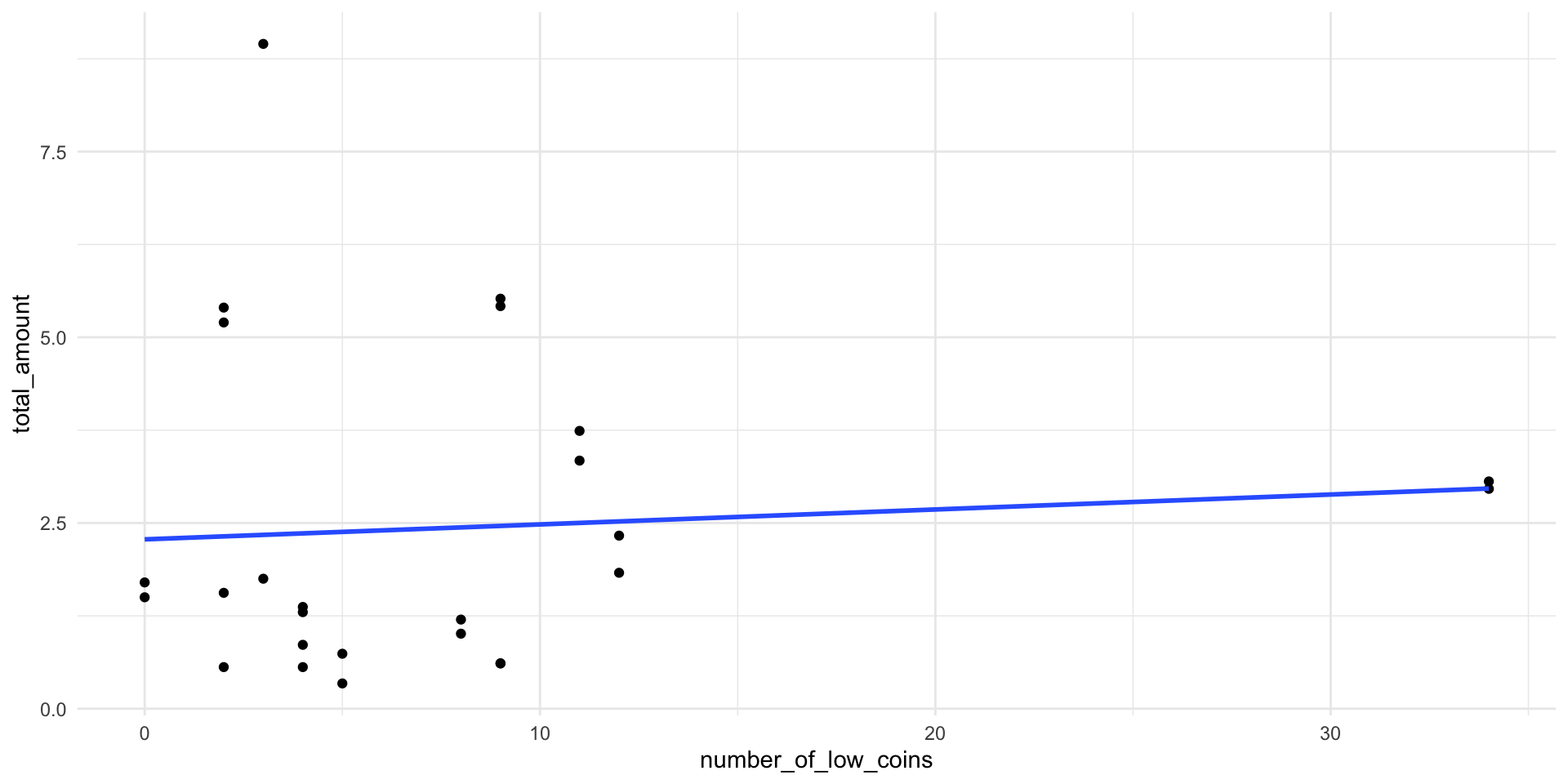

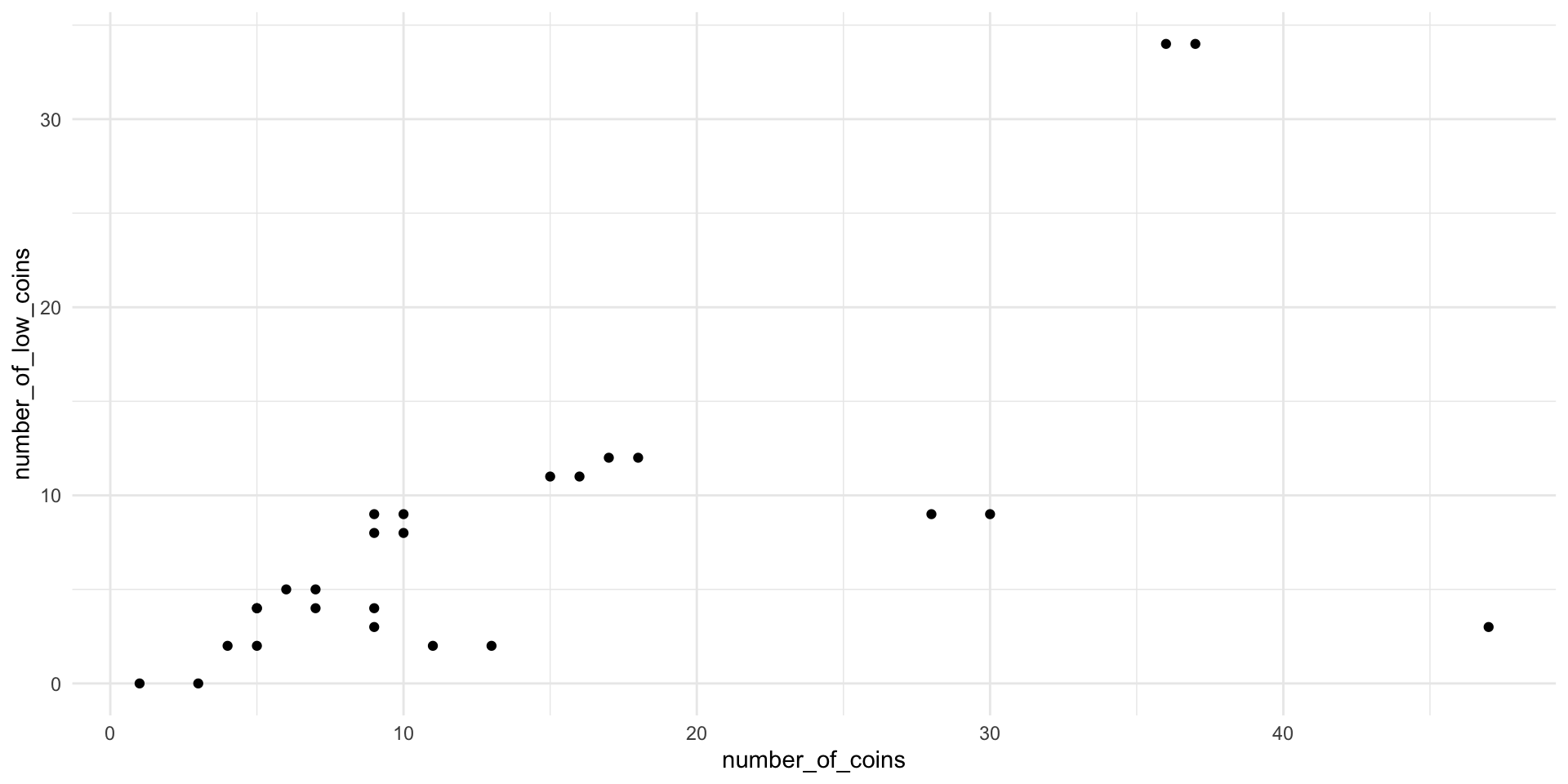

Relationships between the variables

- Of course, there is a relationship between the total amount and each of the predictors

- The number of coins and the number of low coins are also correlated

- Multicollinearity occurs when the predictor variables are correlated with themselves

total_amount vs. number_of_coins.

total_amount vs. number_of_low_coins.

number_of_coins vs. number_of_low_coins.- How is the multiple regression model affected by correlated predictors? \[\begin{array}{rcl}\widehat{total\_amount}&=&0.798 \\ &+& 0.206\times number\_of\_coins\\ &-& 0.160\times number\_of\_low\_coins\end{array}\]

# A tibble: 3 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 0.798 0.301 2.65 1.42e- 2

2 number_of_coins 0.206 0.0209 9.89 9.44e-10

3 number_of_low_coins -0.160 0.0291 -5.51 1.33e- 5\[\begin{array}{rcl}\widehat{total\_amount}&=&0.798 \\ &+& 0.206\times number\_of\_coins\\ &-& 0.160\times number\_of\_low\_coins\end{array}\]

- The relationship between the total amount and each predictor (when considered on its own) is positive

- However, the coefficient for the number of low coins is negative in the multiple regression model

- Why?

Intepreting Coefficients

\[\begin{array}{rcl}\widehat{total\_amount}&=&0.798 \\ &+& 0.206\times number\_of\_coins\\ &-& 0.160\times number\_of\_low\_coins\end{array}\]

- The predicted amount increases by $0.206 for each additional coin, while keeping the number of low coins the same. A quarter is added.

- The predicted amount decreases by $0.160 for each additional low coin, while keeping the number of coins the same. A quarter is replaced by a penny, nickel, or dime.

Multicollinearity

- Multicollinearity is common when there are multiple predictors, especially in observational studies

- Indicates that the predictors include some redundant information

- Makes it difficult to interpret coefficients

- Often results in models with high \(R^2\), but few coefficients significantly different from 0

- Can be avoided with careful experimental design (more on this later)

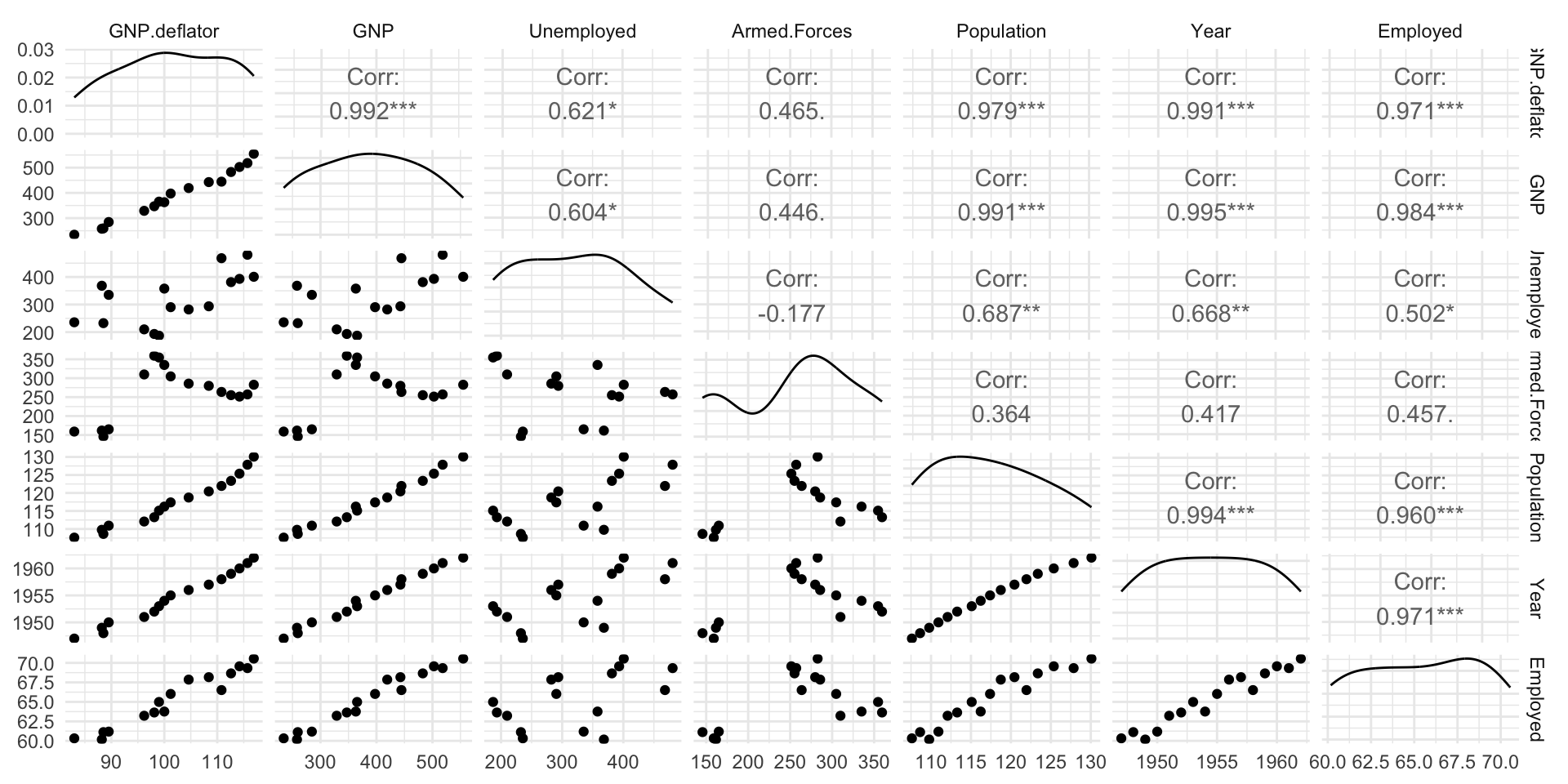

Macroeconomic Data

longleydataset 1- US macroeconomic data from 1947 to 1962 (n = 16)

- Note that observations are dependent, because this is a time series

- Response:

Employed: number of people employed - Predictors:

GNP.deflator: GNP adjusted for inflationGNP: Gross National ProductUnemployed: Number of unemployed peopleArmed.Forces: Number of people in armed forcesPopulation: Noninstitutionalized people at least 14 years old

- Predictors are collinear

Full Model

# A tibble: 7 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -3482. 890. -3.91 0.00356

2 GNP.deflator 0.0151 0.0849 0.177 0.863

3 GNP -0.0358 0.0335 -1.07 0.313

4 Unemployed -0.0202 0.00488 -4.14 0.00254

5 Armed.Forces -0.0103 0.00214 -4.82 0.000944

6 Population -0.0511 0.226 -0.226 0.826

7 Year 1.83 0.455 4.02 0.00304 VIF

- The variance inflation factor (VIF) for the \(i\)th predictor is \[VIF_i=\frac{1}{1-R_i^2}\]

- Here, \(R_i^2\) is the \(R^2\) obtained from for regression of predictor \(i\) in terms of the other predictors

- \(R_i^2\) close to 1 indicates that predictor \(i\) is closely related to the other predictors and is redundant \(\rightarrow\) large \(VIF_i\)

- \(VIF_i>5\) is taken as an indication of collinearity

Variance inflation factors for longley data

Manual Variable Selection

- We can use VIF and p-values to manually reduce the size of the model

- Remove predictors with high VIF, high p-values

- Before we start, note that adjusted \(R^2\) for the full model is 0.992

# A tibble: 1 × 12

r.squared adj.r.squared sigma statistic p.value df logLik AIC BIC

<dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 0.995 0.992 0.305 330. 4.98e-10 6 0.907 14.2 20.4

# ℹ 3 more variables: deviance <dbl>, df.residual <int>, nobs <int>Full Model (6 Predictors)

# A tibble: 7 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -3482. 890. -3.91 0.00356

2 GNP.deflator 0.0151 0.0849 0.177 0.863

3 GNP -0.0358 0.0335 -1.07 0.313

4 Unemployed -0.0202 0.00488 -4.14 0.00254

5 Armed.Forces -0.0103 0.00214 -4.82 0.000944

6 Population -0.0511 0.226 -0.226 0.826

7 Year 1.83 0.455 4.02 0.00304 VIF

GNP.deflator GNP Unemployed Armed.Forces Population Year

135.53244 1788.51348 33.61889 3.58893 399.15102 758.98060 Populationhas a large p-value and large VIF- Eliminate it from the model

5 Predictor Model

# A tibble: 6 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -3565. 772. -4.62 0.000957

2 GNP.deflator 0.0277 0.0607 0.456 0.658

3 GNP -0.0421 0.0176 -2.39 0.0379

4 Unemployed -0.0210 0.00303 -6.95 0.0000397

5 Armed.Forces -0.0104 0.00200 -5.21 0.000397

6 Year 1.87 0.399 4.68 0.000867 VIF

GNP.deflator GNP Unemployed Armed.Forces Year

76.641401 546.870494 14.289620 3.460846 644.626426 GNP.deflatorhas a large p-value and large VIF- Eliminate it from the model

4 Predictor Model

# A tibble: 5 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -3599. 741. -4.86 0.000503

2 GNP -0.0402 0.0165 -2.44 0.0328

3 Unemployed -0.0209 0.00290 -7.20 0.0000175

4 Armed.Forces -0.0101 0.00184 -5.52 0.000180

5 Year 1.89 0.383 4.93 0.000449 VIF

GNP Unemployed Armed.Forces Year

515.123851 14.108642 3.141581 638.128041 GNPhas the largest p-value and large VIF- Eliminate it from the model

Final Model (3 Predictors)

# A tibble: 4 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -1797. 68.6 -26.2 5.89e-12

2 Unemployed -0.0147 0.00167 -8.79 1.41e- 6

3 Armed.Forces -0.00772 0.00184 -4.20 1.22e- 3

4 Year 0.956 0.0355 26.9 4.24e-12VIF

Unemployed Armed.Forces Year

3.317929 2.223317 3.890861 - All predictors have VIF < 5

- All coefficients are significant

- Adjusted \(R^2\) is 0.991, so model describes slightly less variability in employment than the full model

- However, simple model with reduced/no collinearity is preferred

# A tibble: 1 × 12

r.squared adj.r.squared sigma statistic p.value df logLik AIC BIC

<dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 0.993 0.991 0.332 555. 3.92e-13 3 -2.76 15.5 19.4

# ℹ 3 more variables: deviance <dbl>, df.residual <int>, nobs <int>Palmer Penguins

penguinsdataset 1- Measurements for three species of penguins from Palmer Archipelago

- Response:

body_mass_g - Predictors:

species: Adelie, Chinstrap, or Gentoobill_length_mmbill_depth_mmflipper_length_mmsex: female or male

3 Predictor Model

- I performed manual variable selection

- Dropping

speciesandbill_length_mmresulted in all predictors having VIF < 5 and all coefficiencts significantly different from 0

# A tibble: 4 × 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -2247. 625. -3.59 3.76e- 4

2 bill_depth_mm -86.9 15.5 -5.63 3.96e- 8

3 flipper_length_mm 38.2 2.08 18.3 3.47e-52

4 sexmale 538. 51.3 10.5 2.17e-22VIF

bill_depth_mm flipper_length_mm sex

2.653895 2.444470 1.891038 Model Comparison

- Does the simpler 3 predictor model predict

body_mass_gas well as the full model? - We will also compare these two models to the best single predictor model, which uses

flipper_length_mmas the predictor - We would like to compare how well each model performs on data that were not used to train/fit the model

One approach is to compare adjusted \(R^2\)

| Model | predictors | adjusted \(R^2\) |

|---|---|---|

| Full | species, bill_length_mm, bill_depth_mm, flipper_length_mm, sex |

0.873 |

| 3 predictor | bill_depth_mm, flipper_length_mm, sex |

0.844 |

| 1 predictor | flipper_length_mm |

0.758 |

Cross-Validation

- Another approach is to use cross-validation

- Divide the data into fourths (4-fold cross-validation)

- We fit each model 4 times

- Each time we hold out 1/4 of the data and fit the model to the remaining 3/4 of the data

- Use the fitted model to predict

body_mass_gon the 1/4 of the data we held back - Measure the prediction error (residual) on the holdout sample

- Compare models using cross-validation SSE \[CV\,SSE=\sum_{i=1}^n(\hat{y}_{cv,i}-y_i)^2\]

| Model | predictors | CV SSE |

|---|---|---|

| Full | species, bill_length_mm, bill_depth_mm, flipper_length_mm, sex |

28,105,231 |

| 3 predictor | bill_depth_mm, flipper_length_mm, sex |

39,756,521 |

| 1 predictor | flipper_length_mm |

52,576,385 |

- The full model has the smallest CV SSE

- We expect the full model to perform better when predicting

body_mass_gfor penguins that were not used to fit the model